Selecting the right real estate agent can make a world of difference when buying or selling a home. But how do you find the best one? Here are some tips to help you make that big decision as you determine your partner in the process.

Check Their Reputation

Start by gathering information about agents in your area. From there, try to narrow down the list. Ask the people you trust if they have someone they’d recommend. You’ll want to find an agent with a strong online presence, plenty of positive reviews, and someone whose great reputation truly precedes them. As Freddie Mac explains:

“. . . you may want to look for a real estate agent who specializes in the type of home you’re searching for. For example, if you are looking for an energy-efficient home, look for an agent who has experience with finding and negotiating offers for those homes. If you are looking for new construction, you’ll want to find an agent who has experience with new construction and isn’t affiliated with the builder . . .”

Look for Local Market Expertise

A great agent should have in-depth knowledge of what’s happening at the national and local level. That way they can clear up any misconceptions sparked by what you’re reading or hearing in the news. And they can tell you how your area compares to the national data. As an added perk, they’ll also be familiar with the neighborhoods you’re interested in and community amenities. As a recent article from Business Insider says:

“Spend some time talking with prospective agents about the local real estate market and how it could impact your purchase or sale. You want to get an understanding of how knowledgeable they are about local market conditions. Whether they’re helping you sell or buy, their strategy for you should account for those conditions.”

Get a Feel for Their Communication Style and Availability

Effective communication is key in real estate transactions. Choose an agent who listens to your needs, answers your questions quickly, and keeps you informed throughout the process. If an agent is juggling too many clients, they might not be able to give you the attention you deserve. You want someone who will be readily available and responsive. So, what’s the best way to get a feel for their communication style and preferences? Bankrate offers this advice:

“Interviews also give you a chance to find out the agent’s preferred method of communication and their availability. For example, if you’re most comfortable texting and expect to visit homes after work hours during the week, you’ll want an agent who’s happy to do the same.”

Trust Your Gut

Last, rely on your instincts. If you feel like you do or don’t click with one of the agents you’re talking to, that matters. Choose an agent you feel at ease with and who inspires confidence. The right agent should be someone you trust to guide you through one of the most significant transactions of your life. As Business Insider says:

“As long as you’ve properly vetted the agents you’re considering and ensured they have the necessary expertise, it’s ok to go with your gut . . . Maybe you have a better rapport with one of the agents you’re considering, or you just feel like they’re easier to approach. You’re going to be working closely with this person, so it’s important to choose an agent you’re comfortable with.”

Bottom Line

By following these tips, you can pick an agent who’ll provide the support and expertise you need to help make the process as smooth as possible. Connect with local agents to see if they’d be a good fit for working together.

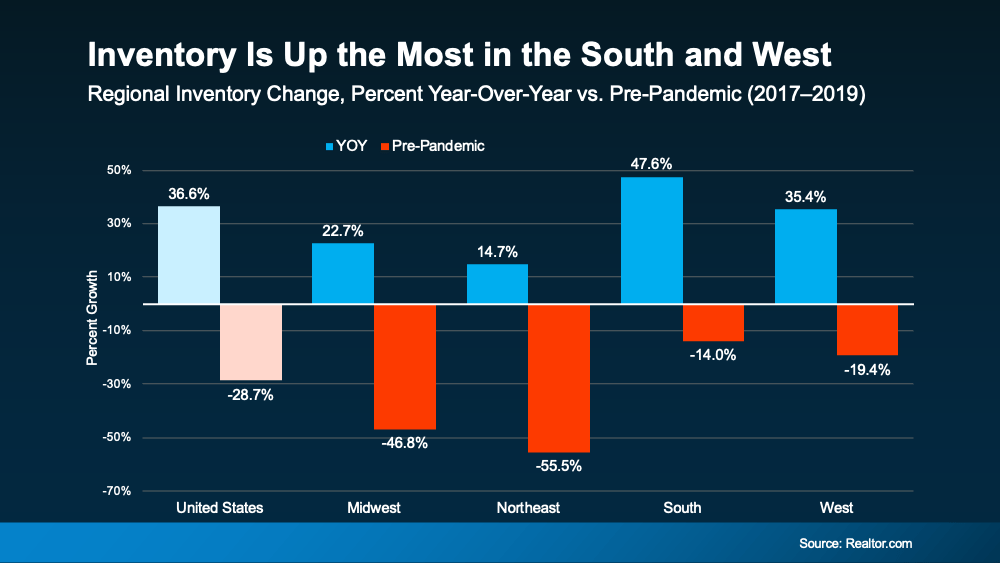

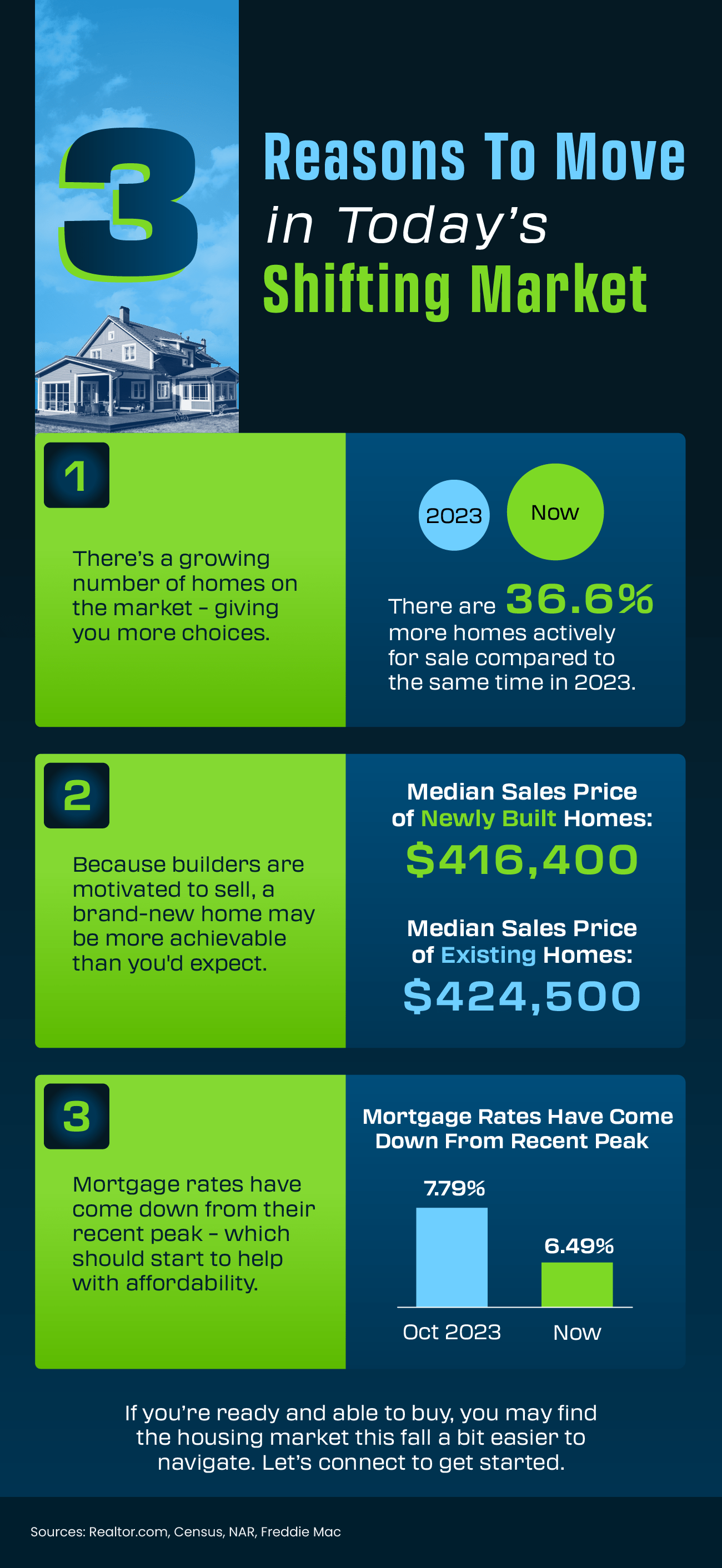

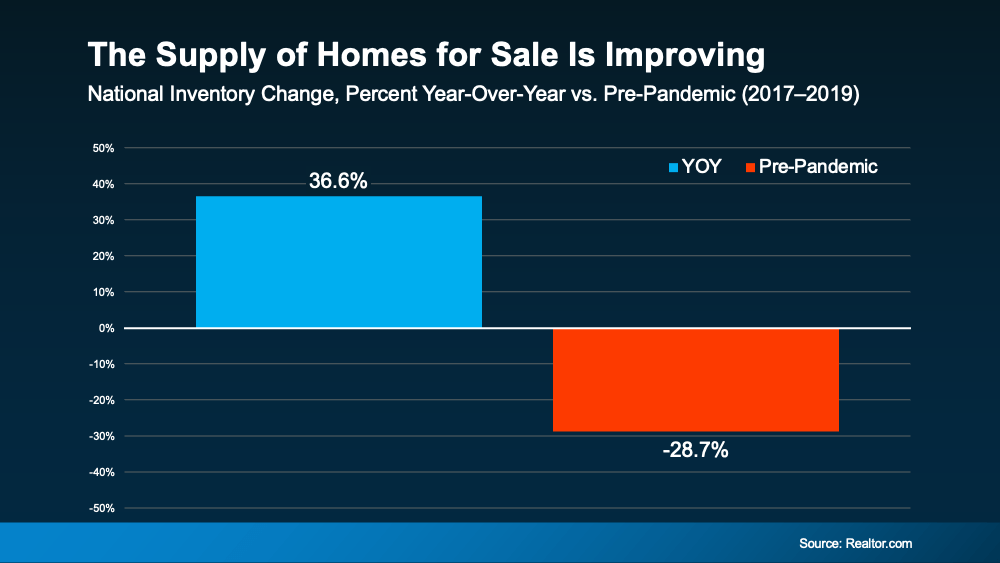

So, while we’re up by almost 37% year-over-year, we’re still not back to how much inventory there’d be in a normal market.

So, while we’re up by almost 37% year-over-year, we’re still not back to how much inventory there’d be in a normal market.