On the road to becoming a homeowner? If so, you may have heard the term pre-approval get tossed around. Let’s break down what it is and why it’s important if you’re looking to buy a home in 2024.

What Pre-Approval Is

As part of the homebuying process, your lender will look at your finances to figure out what they’re willing to loan you. According to Investopedia, this includes things like your W-2, tax returns, credit score, bank statements, and more.

From there, they’ll give you a pre-approval letter to help you understand how much money you can borrow. Freddie Mac explains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Now, that last piece is especially important. While home affordability is getting better, it’s still tight. So, getting a good idea of what you can borrow can help you really wrap your head around the financial side of things. It doesn’t mean you should borrow the full amount. It just tells you what you can borrow from that lender.

This sets you up to make an informed decision about your numbers. That way you’re able to tailor your home search to what you’re actually comfortable with budget-wise and can act fast when you find a home you love.

Why Pre-Approval Is So Important in 2024

If you want to buy a home this year, there’s another reason you’re going to want to be sure you’re working with a trusted lender to make this a priority.

While more homes are being listed for sale, the overall number of available homes is still below the norm. At the same time, the recent downward trend in mortgage rates compared to last year is bringing more buyers back into the market. That imbalance of more demand than supply creates a bit of a tug-of-war for you.

It means you’ll likely find you have more competition from other buyers as more and more people who were sitting on the sidelines when mortgage rates were higher decide to jump back in. But pre-approval can help with that too.

Pre-approval shows sellers you mean business because you’ve already undergone a credit and financial check. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

Sellers love that because that makes it more likely the sale will move forward without unexpected delays or issues. And if you may be competing with another buyer to land your dream home, why wouldn’t you do this to help stack the deck in your favor?

Bottom Line

If you’re looking to buy a home in 2024, know that getting pre-approved is going to be a key piece of the puzzle. With lower mortgage rates bringing more buyers back into the market, this can help you make a strong offer that stands out from the crowd.

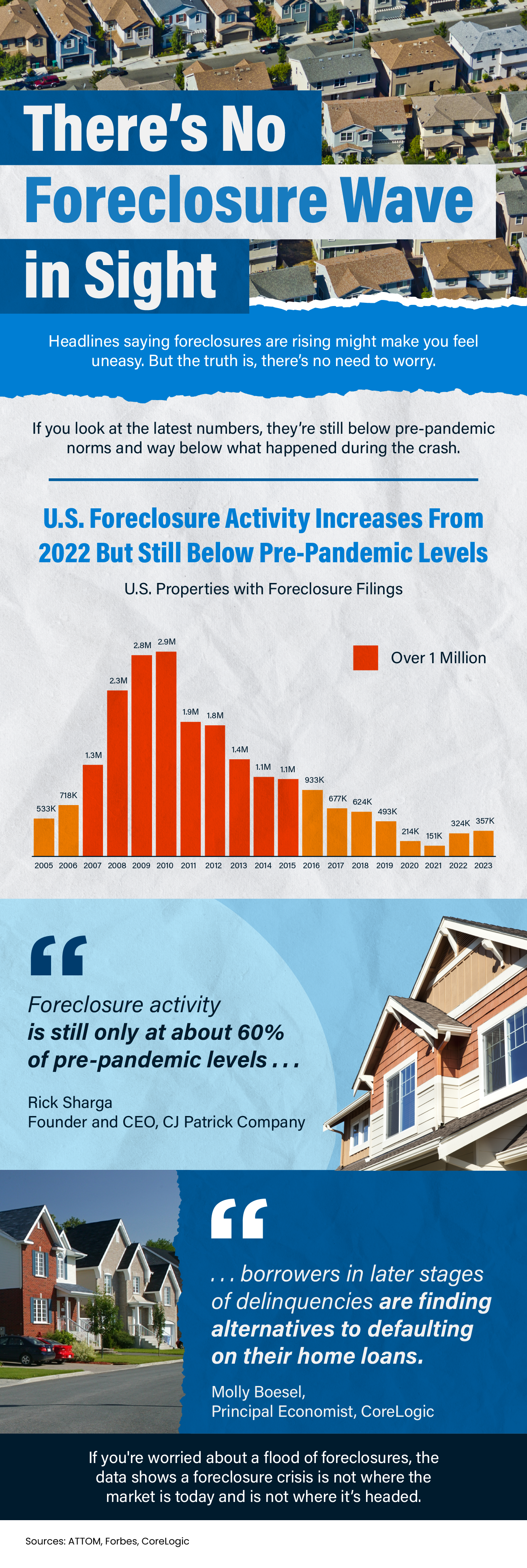

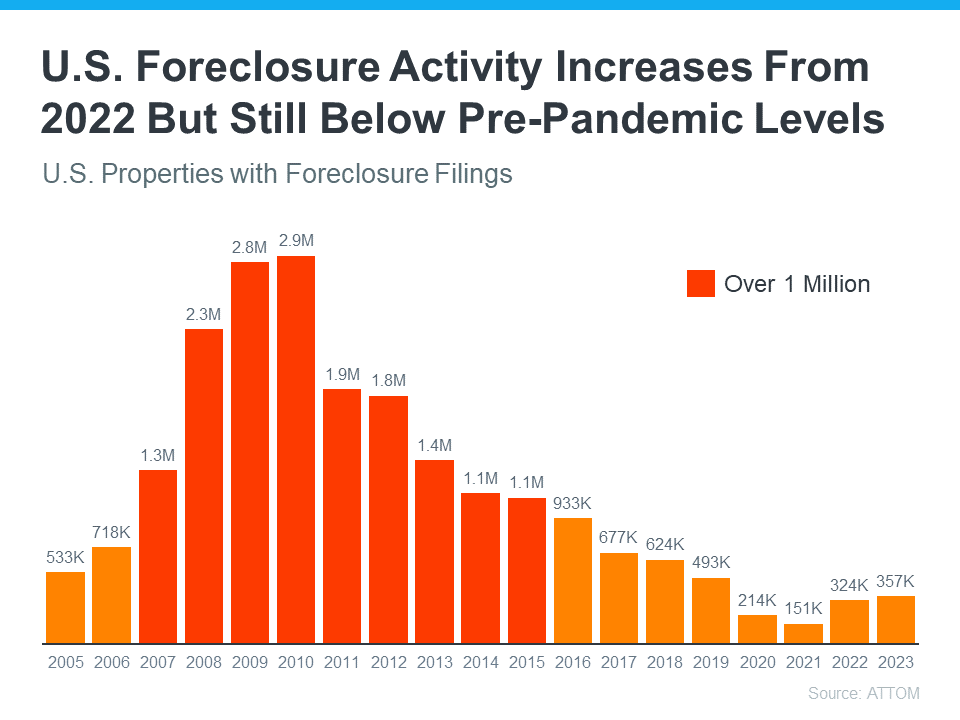

![There’s No Foreclosure Wave in Sight [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/KeepingCurrentMatters/content/images/20240201/Theres-No-Foreclosure-Wave-in-Sight-KCM-Share.png)

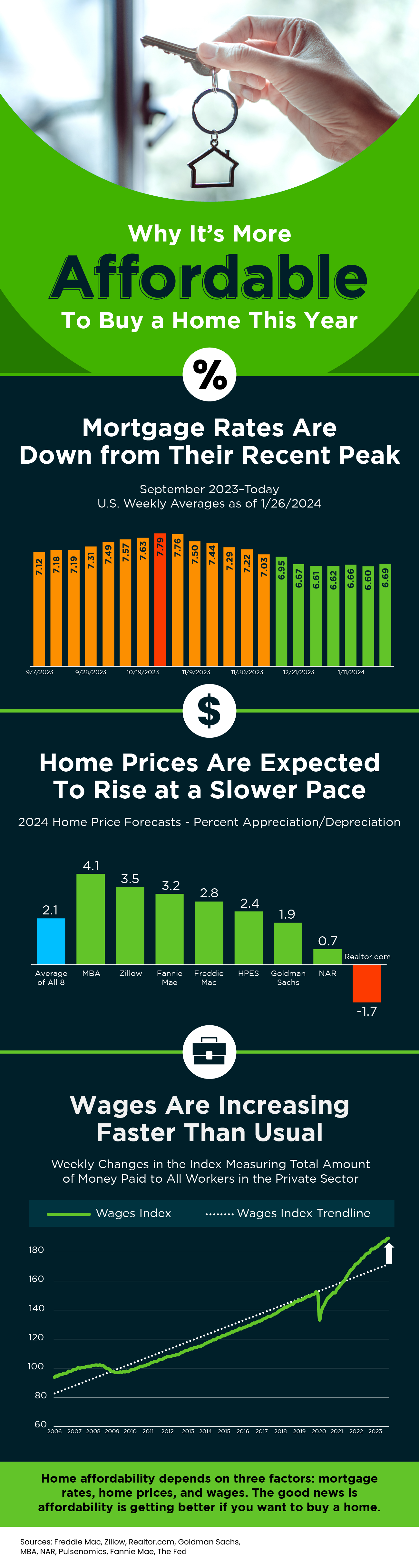

![Why It’s More Affordable To Buy a Home This Year [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/KeepingCurrentMatters/content/images/20240125/202401-1.PNG)