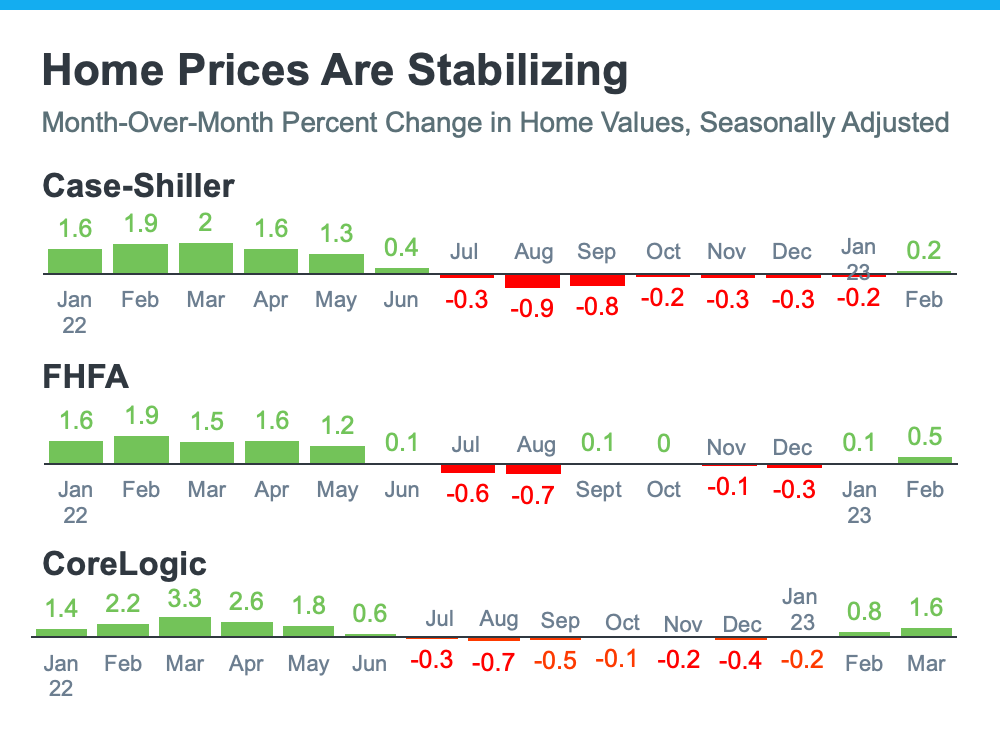

The National Association of Realtors (NAR) will release its latest Existing Home Sales Report tomorrow. The information it contains on home prices may cause some confusion and could even generate some troubling headlines. This all stems from the fact that NAR will report the median sales price, while other home price indices report repeat sales prices. The vast majority of the repeat sales indices show prices are starting to appreciate again. But the median price reported on Thursday may tell a different story.

Here’s why using the median home price as a gauge of what’s happening with home values isn’t ideal right now. According to the Center for Real Estate Studies at Wichita State University:

“The median sale price measures the ‘middle’ price of homes that sold, meaning that half of the homes sold for a higher price and half sold for less. While this is a good measure of the typical sale price, it is not very useful for measuring home price appreciation because it is affected by the ‘composition’ of homes that have sold.

For example, if more lower-priced homes have sold recently, the median sale price would decline (because the “middle” home is now a lower-priced home), even if the value of each individual home is rising.”

People buy homes based on their monthly mortgage payment, not the price of the house. When mortgage rates go up, they have to buy a less expensive home to keep the monthly expense affordable. More ‘less-expensive’ houses are selling right now, and that’s causing the median price to decline. But that doesn’t mean any single house lost value.

Even NAR, an organization that reports on median prices, acknowledges there are limitations to what this type of data can show you. NAR explains:

“Changes in the composition of sales can distort median price data.”

For clarification, here’s a simple explanation of median value:

- You have three coins in your pocket. Line them up in ascending value (lowest to highest).

- If you have one nickel and two dimes, the median value of the coins (the middle one) in your pocket is ten cents.

- If you have two nickels and one dime, the median value of the coins in your pocket is now five cents.

- In both cases, a nickel is still worth five cents and a dime is still worth ten cents. The value of each coin didn’t change.

The same thing applies to today’s real estate market.

SBottom Line

Actual home values are going up in most markets. The median value reported tomorrow might tell a different story. For a more in-depth understanding of home price movements, reach out to a local real estate professional.

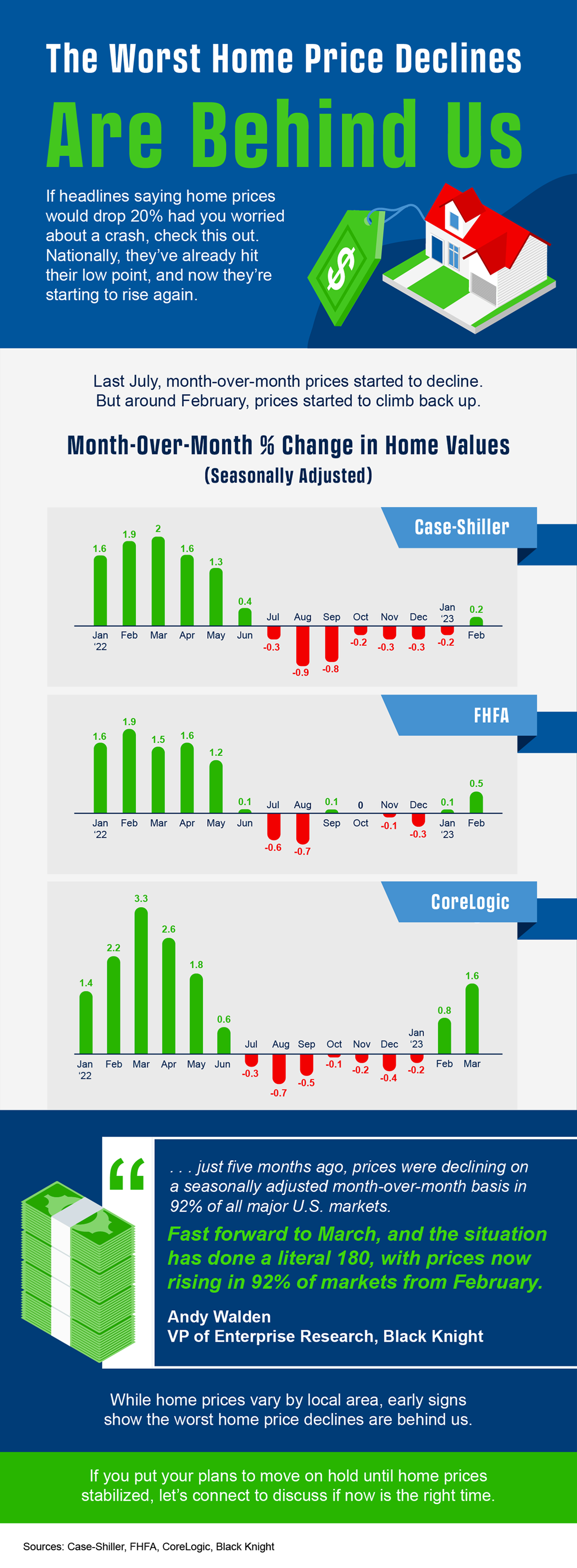

![The Worst Home Price Declines Are Behind Us [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230511/The-Worst-of-Home-Price-Declines-Are-Behind-Us-KCM-Share.png)

![Reasons To Sell Your House Today [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230504/Reasons-To-Sell-Your-House-in-Todays-Market-KCM-Share.png)